The European battery storage market is at an inflection point. With Chinese lithium-ion battery prices dropping 45% in 2025 and complete systems landing at under €100/kWh, what does this mean for second-life EV batteries? We analyse the real economics of battery reuse in Europe — the landed costs, the processing margins, and what separates the companies making second-life work from those who've walked away.

How Low Have Prices Actually Gone?

Complete battery systems from Chinese manufacturers are landing in Europe at prices that would have seemed implausible eighteen months ago.

DIY solar forums report floor prices touching $62/kWh for 48V systems. Docan is shipping 120kWh systems with EVE cells for $11,000 — that's $92/kWh, integrated, certified, delivered. Prices so low that even DIY Solar communities are questioning if they're real.

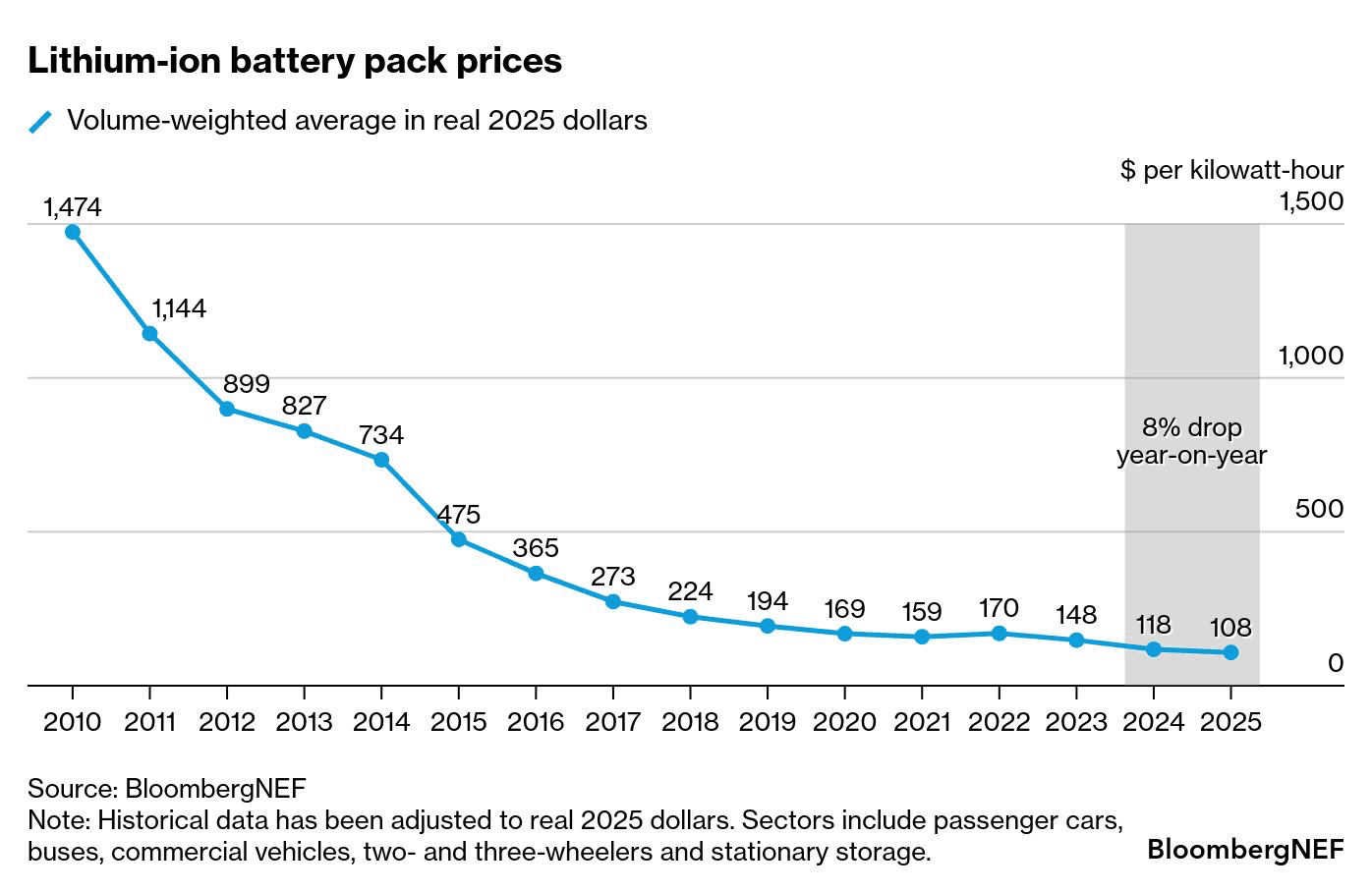

BloombergNEF's December 2025 survey found global stationary storage packs at $70/kWh — down 45% in a single year. In China, it's even starker: 60 of 76 bidders in PowerChina's 16GWh tender came in under $68/kWh.

The overcapacity is structural. Global battery manufacturing capacity reached 3 TWh in 2024 — three times actual demand. China holds 85% of that capacity. When supply outstrips demand threefold, prices don't fall. They collapse.

What European Buyers Are Actually Paying

Forget the headlines. What does this mean for real buyers? We've consulted live prices from European installers selling reputable Chinese energy storage brands.

Residential & Small Commercial (20–30 kWh)

| Brand | Price (€/kWh) |

|---|---|

| Sunways | ~€150 |

| Enershare | ~€150 |

| Pylontech Force H3 | ~€180 |

| Marstek | €190–200 |

Typical range: €140–170/kWh

Large Commercial (60–200+ kWh)

| Brand | System Size | Price (€/kWh) |

|---|---|---|

| Deye | 50–100 kWh | €150–155 |

| Dyness | 50–100 kWh | ~€160 |

| Growatt | 50–100 kWh | €170–190 |

| KSTAR | 50–100 kWh | €200+ |

| Solax | 1 MWh | €133–135 |

| V-TAC | 100 kWh | €50–60 |

The V-TAC pricing is the real outlier here.

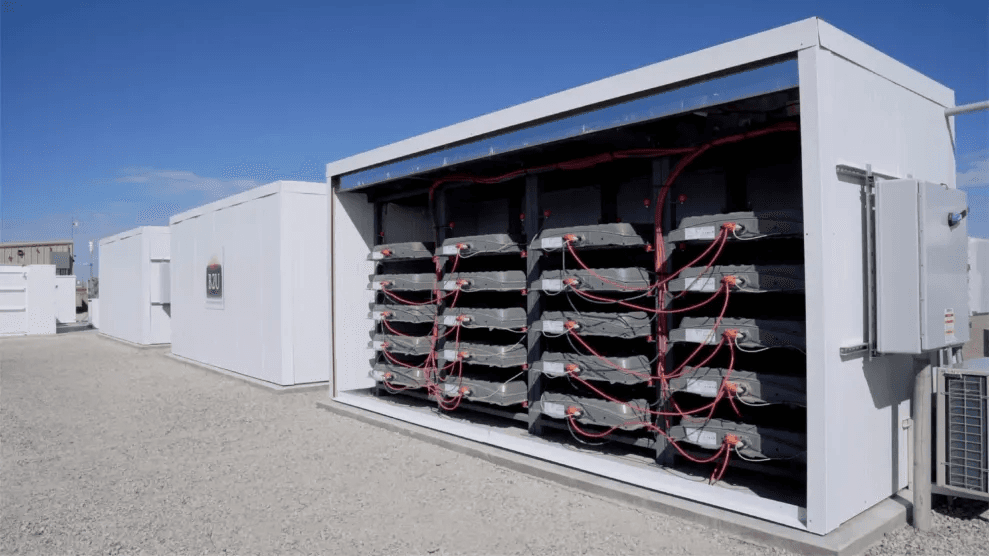

Containerised (200+ kWh)

| Source | Price |

|---|---|

| Utility-scale BESS (outside China/US) | ~€115/kWh total project cost; core equipment ~€70/kWh (Ember) |

| Tesla Megapack (Europe) | ~€225/kWh — premium pricing for a premium product |

The Second-Life Economics Question

Here's where it gets interesting for the reuse market.

Second-life EV packs typically trade at €15–50/kWh in Europe, depending on chemistry, condition, and volume. That's your starting point.

The harder question: what does it actually cost to turn a raw pack into a deployable system?

- Testing and grading

- Reject rates

- BMS integration

- Enclosure and assembly

- Certification

- Warranty reserve

Running the Numbers

Optimistic scenario

| Line item | Cost |

|---|---|

| Raw packs | €30/kWh |

| Processing | €50/kWh |

| Total | €80/kWh ✓ price-competitive |

Realistic European scenario

| Line item | Cost |

|---|---|

| Raw packs | €30/kWh |

| Processing (transport, compliance, labour) | €80/kWh |

| Total | €110/kWh — on par with aggressive Chinese pricing |

The viability question is simple: is the gap between raw pack cost (€15–50/kWh) and new system cost (€110–190/kWh) wide enough to cover processing, deliver margin, and give buyers a reason to choose used?

The Reality Check

I've spoken to two companies that were building energy storage systems with second-life packs. Both have stopped. They've pivoted to new cells. The economics didn't hold.

But others are making it work — which raises the question: what's different?

What Separates the Winners?

Companies like Allye, Rebaba, upVolt, and Connected Energy are building real second-life systems, serving real customers, generating real revenue. The path exists.

What separates them? From what I can see, one driver stands out: supply chain control.

- Consistent pack types

- Predictable quality

- Reliable volume

With that foundation, you can build repeatable processes and actual margins. Without it, every project becomes a custom engineering exercise — and custom doesn't scale.

Where This Leaves the Market

Chinese cell prices will likely keep falling. But here's the counterintuitive bit: as new systems get cheaper, raw second-life pack prices often fall too — since second-life pricing is frequently anchored to new.

The €100–150/kWh gap between feedstock and finished systems doesn't necessarily compress. It may even hold. That's workable margin for operators who've figured out efficient processing.

The Bottom Line

The business model is there. Falling EV pack prices aren't a threat to second-life — they're the feedstock getting cheaper.

The operators who secure consistent supply at today's prices and build efficient remanufacturing workflows will capture that spread.

And second-life won't win every deal on price alone. It doesn't need to. It needs to win the deals where documentation, traceability, and local supply matter — and those deals are growing.